The Final State of the Union

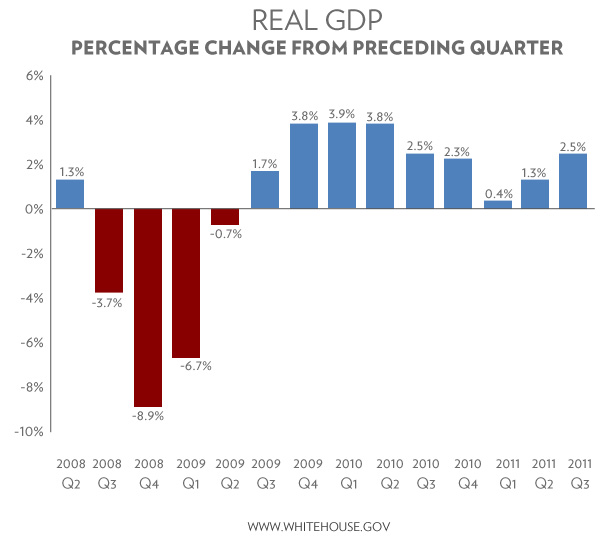

Today’s report shows that the economy posted the ninth straight quarter of positive growth, as real GDP (the total amount of goods and services produced in the country) grew at a 2.5 percent annual rate in the third quarter of this year. The level of real GDP now exceeds its level at the business cycle peak in the fourth quarter of 2007. While the continued expansion is encouraging, faster growth clearly is needed to replace the jobs lost in the recent downturn and to reduce long-term unemployment.

Notable strength in the third quarter included business investment, which grew 16.3 percent at an annual rate. Residential construction increased 2.4 percent at an annual rate, and was up 1.6 percent during the past four quarters, the first positive four-quarter percent change since 2006 except for a brief period when the home buyer tax credit was active. Positive contributions to real GDP growth included consumer spending (1.7 percentage point), fixed investment (1.6 percentage point), and net exports (0.2 percentage point). Inventory investment subtracted 1.1 percentage point from real GDP growth.

We are, nonetheless, at a fragile moment in the world economy, and cannot afford to do anything to undermine our economic recovery. That’s why the President continues to urge Congress to pass the American Jobs Act without delay. The American Jobs Act includes measures that would accelerate the recovery, including extending the payroll tax cut and unemployment insurance, keeping teachers in the classroom and police and firefighters on the beat, and investing in our nation’s infrastructure to help put Americans back to work. Independent economists say it could increase employment by up to 1.9 million, increase growth and lower the unemployment rate. This report also underscores the need to put in place a balanced approach to deficit reduction that phases in budget cuts, instills confidence, and allows us to live within our means without shortchanging future growth.

.